National Payments Corporation of India: A Deep Dive into its Role

- What is NPCI?

- Recent Announcements from NPCI

- Leadership & Governance: Who Runs NPCI?

- Core Objectives Behind NPCI’s Initiatives

- Why NPCI is Critical to India’s Cashless Economy?

- How NPCI Facilitates Payment Processing?

- Popular Services Offered by NPCI

- How to Use NPCI Platforms?

- Easy Ways to Reach NPCI for Support and Complaints

- Simplifying eCommerce Payments with Shiprocket Checkout

- Conclusion

Over the past ten years, payment practices in India have undergone significant changes. For millions, using UPI, scanning a QR code, or tapping a phone has become second nature. The main force behind this gradual and silent change is the NPCI (National Payments Corporation of India). According to NPCI’s March 2024 data, UPI alone handled over 13 billion transactions in a single month, totaling ₹19.78 lakh crore.

Private companies do have a role here, but the NPCI is the glue keeping it all together. Everyone including banks, apps, companies, and everyday users has profited from what NPCI has created.

Read further to find out how the government agency, NPCI, has improved trust, simplified payments, and managed routine finances.

What is NPCI?

The National Payments Corporation of India was incorporated in 2008 to facilitate scalable unified payment infrastructure across the country. It works under the guidance of two bodies: the Indian Banks’ Association and the Reserve Bank of India. The main goal of this authority is to make payment systems in the country safer, quicker, and easily accessible to everyone.

NPCI’s job is more about public service as compared to private firms chasing profits. It sets up and maintains key systems that banks and digital wallets use, like UPI, IMPS, and RuPay. These are payment methods most Indians rely on for transactions.

Recent Announcements from NPCI

NPCI regularly makes updates to enhance the security, efficiency, and reliability of digital payments. Here are some of the major recent declarations:

Third-Party App Approval

On December 31, 2024, NPCI announced an extension of the deadline for third-party app providers (TPAPs) like PhonePe and Google Pay to comply with the 30% market share cap on UPI transactions. The new deadline is December 31, 2026.

This means such payment apps can keep serving a large chunk of UPI users while newer players are given room to grow.

UPI Internationalisation

Another announcement that made headlines was the push for UPI internationalisation. The goal here is to make Indian travellers and NRIs feel just as comfortable paying abroad as they do at home.

February 21, 2023: UPI and Singapore’s PayNow launched cross-border transactions, allowing users in both countries to send and receive funds seamlessly.

February 2, 2024: NPCI and France’s Lyra Network officially launched UPI acceptance at the Eiffel Tower, enabling Indian tourists to make payments using UPI.

March 29, 2024: PhonePe announced UPI payments acceptance at NeoPay terminals in the UAE, facilitating transactions for Indian users abroad.

July 3, 2024: UPI is officially accepted in countries including Nepal, Sri Lanka, Mauritius, UAE, Singapore, France, and Bhutan.

Increased Transaction Limits

On December 8, 2023, the Reserve Bank of India (RBI) announced an increase in the UPI transaction limit for payments to educational institutions and hospitals from ₹1 lakh to ₹5 lakh. NPCI directed banks and payment service providers to implement this change by January 10, 2024. This change helps people make large, necessary payments in one go through UPI instead of relying on cash or cheques.

Leadership & Governance: Who Runs NPCI?

NPCI is not led by one single body. It is run as a not-for-profit organisation, with a group of public and private banks as stakeholders. It has a board of directors comprising experts from finance, tech, and banking backgrounds. This team is responsible for approving new systems, updating old ones, and making sure the digital payment scene in India stays safe and inclusive. Since it works differently than a private firm, the focus is more on long-term benefits than quick wins.

Core Objectives Behind NPCI’s Initiatives

The National Payments Corporation of India has clear objectives, which entail the following:

- The NPCI wants to make the process of everyday payments quick and secure. To do this, it builds simple, low-cost systems that banks and apps can use across cities, towns, and villages.

- It aims to make digital payments accessible to all, not just those with smartphones. Its tools, like UPI, are built to work even on basic phones, helping people in smaller towns and rural areas stay connected.

- NPCI aspires to reduce reliance on cash to make the Indian economy cleaner and easier to track, a win-win situation for the government and the public.

Why NPCI is Critical to India’s Cashless Economy?

A cashless system needs a trusted base that connects banks, mobile apps, merchants, and users. This is where NPCI steps in.

For example, UPI wouldn’t exist without NPCI’s work. It connects over 400 banks and fintech companies to make real-time payments possible. This system processes over 10 billion transactions each month (processed over 16.58 billion UPI transactions in October 2024), which shows how deeply NPCI is tied to the country’s digital payment revolution.

It doesn’t stop at UPI. With services like Bharat BillPay and the Aadhaar-enabled Payment System (AePS), NPCI brings digital access to people in villages, along with urban areas.

How NPCI Facilitates Payment Processing?

Every time someone pays using UPI or scans a QR code for payment, there’s a fast, behind-the-scenes system at work. NPCI runs this system, making sure the money reaches the right place without delays or errors.

Here’s how it all works:

- When you scan a QR code to pay, a lot happens in seconds. NPCI’s systems manage the routing of that payment, confirming the money leaves the sender’s bank and reaches the receiver’s account. And all this is done within moments, 24/7.

- Its setup handles lakhs of payments every minute. NPCI avoids the mess of multiple one-on-one connections between banks by using a central model that banks and apps connect to. This is what makes services like UPI and IMPS so reliable and fast.

- Security checks are built into the process. Fraud filters, OTP verifications, and device-level checks are part of how NPCI keeps things safe. The system is built to grow, as more users come in, it adds capacity without slowing down.

Popular Services Offered by NPCI

Here are some services from NPCI that many people use in India:

UPI (Unified Payments Interface): It’s the most used digital payment tool in India today. It links 673 live banks (banks fully connected and actively working with UPI) and multiple bank accounts, allowing real-time payments and transfers through mobile.

RuPay: This is practically a card network similar to Visa and Mastercard but made in India. It works for credit, debit, and prepaid transactions, and is connected with 1,297 live banks currently.

IMPS (Immediate Payment Service): It lets you send money instantly, even outside normal banking hours. IMPS has about 947 member banks, which are officially part of this payment network and are set up to offer IMPS service. It includes both public and private banks that have signed up and integrated the system into their platforms.

Bharat BillPay: An easy way to pay bills from any platform or app that supports it.

AePS (Aadhaar Enabled Payment System): This payment service has 153 live entities (organisations currently active and processing Aadhaar-based transactions). AePS allows remote-area users to access their bank accounts using their Aadhaar number and fingerprint.

BHIM (Bharat Interface for Money): A mobile app that enables simple, easy, and quick payment transactions using UPI. Users can make instant bank-to-bank payments and collect money with just a mobile number or Virtual Payment Address (VPA).

Bharat QR: A common QR code standard developed jointly with international card schemes. Merchants can display these QR codes, and customers can pay through various methods by scanning them via Bharat QR-enabled applications.

NETC FASTag: It’s an electronic toll collection system that permits toll charges to be automatically deducted, allowing cars to drive through toll plazas without pausing to pay with cash.

e-RUPI: A digital voucher system that facilitates contactless and cashless transactions. It guarantees welfare services are delivered without leaks.

The National Automated Clearing House, or NACH Credit: It’s a web-based platform that makes it easier to conduct high-volume, repetitive, and periodic electronic transactions between banks.

*99# (USSD-based Mobile Banking): This service allows transactions without requiring internet connectivity, bringing banking services to all regular mobile phone users.

BHIM Aadhaar: A payment interface that enables businesses to accept digital payments from clients by using their biometric authentication and Aadhaar number.

CTS (Cheque Truncation System): An image-based clearing system that eliminates the need to move physical cheques from one bank to another, speeding up the cheque clearing process.

National Financial Switch (NFS): This network facilitates interbank ATM transactions by linking all of the nation’s ATMs.

APBS (Aadhaar Payment Bridge System): This system electronically credits government subsidies and benefits to the intended beneficiaries’ Aadhaar-linked bank accounts using their Aadhaar numbers.

Electronic Know Your Customer (e-KYC) services: These services enable banks and other financial institutions to digitally confirm the identity of their clients.

Autopay: This function enables users to program automatic payments for services such as utility bills, loan EMIs, and subscriptions, guaranteeing on-time payments without the need for human involvement.

How to Use NPCI Platforms?

The National Payments Corporation of India has many services and they are pretty easy to use.

- UPI Interface: You can accept UPI payments through apps like Google Pay, PhonePe, Paytm, and others. Your customers just scan your QR code or enter your UPI ID to pay.

- RuPay: Using the RuPay card network, you can accept online and offline payments from customers through credit/debit cards.

- BHIM Aadhaar Pay: This one’s helpful if you serve customers in rural areas. Customers can pay you using their Aadhaar number and fingerprint/biometrics, and won’t need their card or phone.

- Other Services: If you run a larger operation, NPCI also supports ATM transactions through the National Financial Switch (NFS), and bulk transfers like salaries or refunds through the National Automated Clearing House (NACH).

Easy Ways to Reach NPCI for Support and Complaints

Here’s how you can make a complaint when you experience an issue with UPI or any other NPCI service:

For UPI Issues:

- Go to the NPCI website.

- Under ‘Get In Touch’, pick ‘UPI Complaint’.

- Enter your details, choose the problem type (like transaction error, login issue, etc.), and press submit. Someone from NPCI will get back to you by email or phone.

Regarding Other Services (like RuPay, IMPS, AePS, or NFS ATM):

- Visit the same NPCI website.

- Select the product you’re having trouble with, fill out the form, and send it. The support team will follow up to help sort it out.

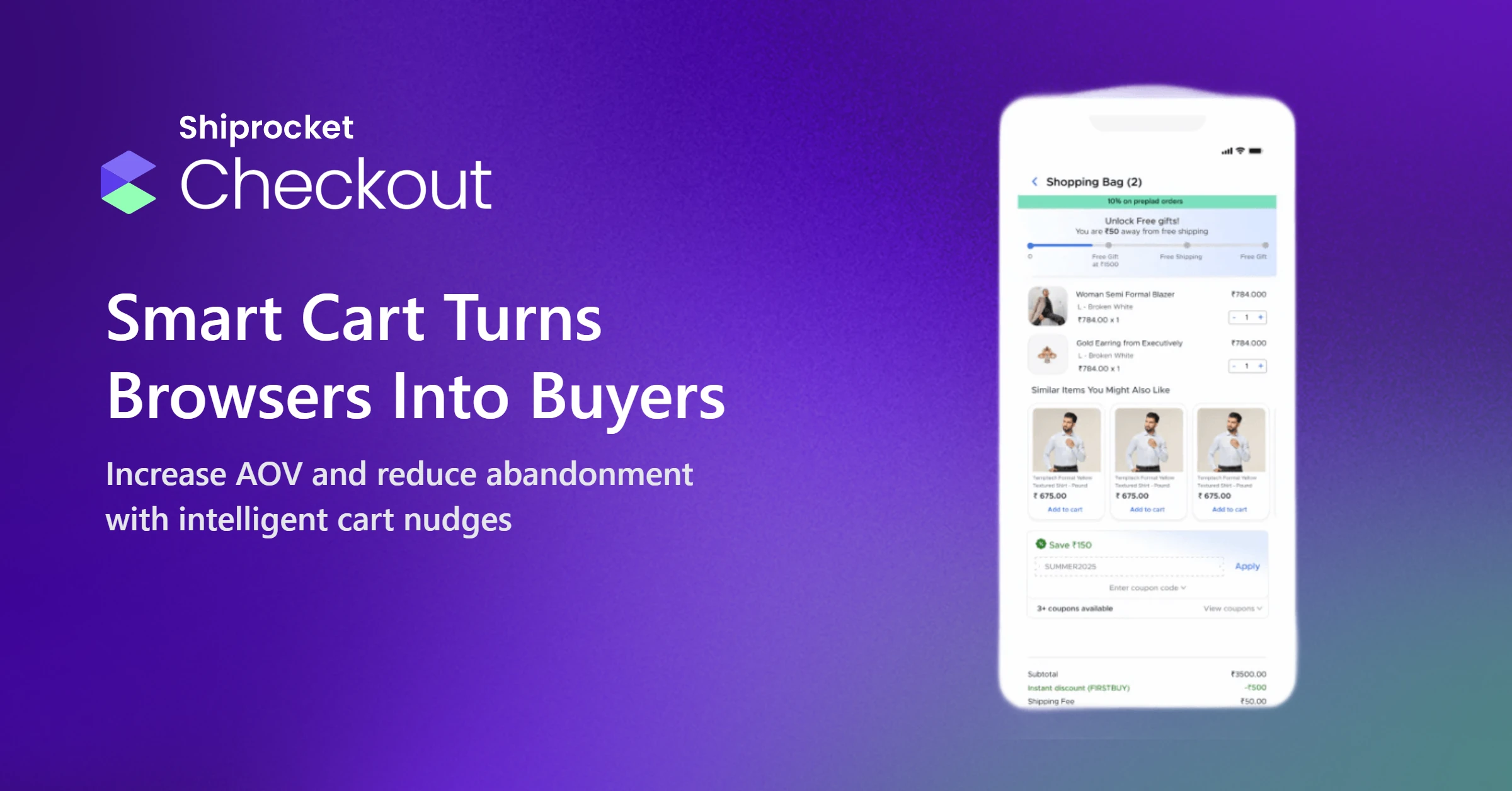

Simplifying eCommerce Payments with Shiprocket Checkout

eCommerce sellers and buyers often face trouble with payments, like failed checkouts, delays in refunds, or lack of trust in the process. Shiprocket Checkout helps fix that.

Your customers can conveniently pay using UPI, cards, wallets, or other NPCI-backed methods once they get to the checkout page.

Shiprocket Checkout integrates with NPCI-built tools to make customer transactions quick and transparent. Such a fast and reliable checkout and payment process can also reduce your cart abandonment rates by 25%.

If you’re looking to grow your eCommerce business, this kind of support system makes a big difference.

Conclusion

The National Payments Corporation of India may not be a household name, but its work touches almost every digital payment made in the country. From customers paying for groceries to buying flight tickets online, it’s highly possible that NPCI’s systems are behind the completion of those payments.

With Indian customers trusting digital payments more than ever, NPCI has become an important part of our country’s financial backbone. With steps to go global, its impact could stretch far beyond Indian borders soon.