The Basics of Failed Payment Recovery Every Business Should Know

Failed payments might sound like a small hiccup, but they can quickly accumulate and become a significant problem for businesses that rely on regular transactions. Payment failures range from 5% to 10% worldwide, depending on the location and payment method used. You’d be surprised to know that these failed payment attempts cost companies around $20.3 billion globally every year.

Regardless of whether you have a subscription-based service, an eCommerce store, or a digital product platform, failed payments mean lost income, frustrated customers, and even cancelled services. About 33% of shoppers who experience a payment failure are unlikely to try again or return to your e-store. That’s why having an effective process for recovering failed payments is something you should consider.

As you read on, you’ll understand what causes failed payments, how to find trouble in your system early, and what you must do next.

What Causes Failed Payments?

Payment attempts can fail for various reasons, as every business has its way of handling billing, card details, and payment systems. Here’s a look at the most frequent ones:

Customer-Related Payment Issues

- Not enough money in the account: This is one of the biggest causes of failed payments. People sometimes don’t realise they’ve gone over their card limit or don’t have enough balance to complete the payment.

- Outdated cards: A customer might try to pay with an old card that’s already expired, especially if they haven’t updated their details after receiving a new one.

- Blocked by fraud checks: Some payments are declined even when they are genuine. This happens when banks or card networks flag the purchase as unusual, such as when a person makes a large purchase or shops from a new location.

- Wrong card details: If someone enters the card number, CVV, expiration date, or billing address incorrectly, the payment will not go through.

- Credit limit reached: If a person is using a credit card and has already spent most of their available limit, the payment may not go through.

- Internet or device problems: A slow connection or an error on the customer’s device can also interrupt the payment process before it is complete.

- Spending caps from banks: Some banks place daily or weekly limits to protect users from fraud. These rules can sometimes stop even regular payments from being completed.

Business-Side Payment Issues

- Website or system errors: Glitches in the checkout process or on the server can stop payments from being processed.

- Obsolete/Old software: If the business is running an outdated version of its checkout software or eCommerce platform, it could lead to payment failure.

- Currency problems: If someone tries to pay in a currency the business doesn’t support, the transaction might be blocked.

- Incorrect payment gateway setup: If the business hasn’t set up the payment gateway properly, it may not be able to handle transactions correctly.

- Recurring payment failures: If the payment is for a subscription or renewal, it may fail if the customer’s card has expired or their balance is insufficient.

- Built-in security rules: Sometimes, a business sets up filters or blocks to prevent frauds, but these can also block genuine payments.

- Billing address mismatch: If the address saved on the user’s account doesn’t match the one on their bank records, the transaction may be stopped.

Payment Processor-Related Payment Problems

- Platform outages: Sometimes, the problem is outside both the business and the customer. If the payment processor is down, no payments can be handled during that time.

- Too much traffic: During festive sales or busy periods, the payment processor may struggle to keep up with the number of transactions, resulting in errors or delays.

- Connection failures: If there is a break in the link between the business’s site and the payment processor, it can cause failed payments even when everything else appears fine.

- Mistaken fraud blocks: Like banks, payment processors also use automated checks to detect fraud. These can sometimes wrongly flag and stop a valid transaction.

Other Possible Reasons

- Cross-border payments: International payments can fail more frequently due to currency conversions, additional checks, or card rules in different countries.

- Chargebacks: If a customer reports a payment as suspicious, their bank might reverse the transaction. This can result in a failed payment even after it was approved earlier.

- Third-party plugin issues: Many online shops use extra tools or plugins for taxes, delivery or discounts. If one of these tools has a problem, it can also affect the payment process.

How to Track Down Failed Payment Issues in Your System

Finding the cause gives you a better chance at fixing issues early and improving your chances of successful transactions. Below are some ways to know where the trouble might be coming from:

Start With the Decline Code

Each time a card transaction fails, your payment processor will usually show a decline code. This code helps explain why the payment didn’t go through. Some common reasons for this include expired cards, incorrect details, or a bank blocking the charge.

Checking this first gives you a clear starting point, especially if you’re looking into individual failed payments.

Review Your Fraud Filters

Fraud protection tools are useful, but sometimes they mistakenly flag genuine payments. Go through your current fraud settings to see if any filters are set too strictly. If real customers are being blocked, you may need to adjust your rules to allow smoother transactions without affecting security.

Notice Patterns in Your Payment Data

Try to find trends after collecting all the information from your payment gateway and fraud settings. See if customer payments are failing during a set time period of the day, or if one payment method fails more than others. It could also be that transactions from some specific regions or locations are blocked.

Getting hold of these patterns can give you a clear picture of the main issue and help you put a stronger failed payment recovery process in motion.

Closely check your payment gateway.

If you see a lot of transactions failing, your payment gateway may have some issues. So, check your integration setup thoroughly and review the logs to see which transactions are not going through and why.

Sometimes, the problem is easy to catch, like one method or region showing a high failure rate. If you don’t get anything easily, then collect as much data as you can to find the root cause.

What to do After a Payment Fails: Recovery Strategies That Work

After you’ve found a failed transaction, you must take corrective action. Here’s what you can do to practically recover the payment:

Retry the payment automatically: It’s one of the easiest things you can do to manage failed payment recovery. Many payment systems let you set up automatic retries after a failed charge. Timing matters; trying again within 24 to 48 hours usually works better than waiting too long.

Send clear and friendly reminders: Reach out to your customer with a helpful message. Let them know their payment didn’t go through and offer a link to update their card details. You must keep the tone light and supportive because no one likes a stern payment warning in their inbox.

Offer multiple payment options: If a customer’s card keeps failing, they may want to use an alternative payment methods, such as split payments, UPI, net banking, or digital wallets. The more payment choices you offer, the more chances they have to pay or retry successfully.

Use advanced payment recovery tools: Many platforms have built-in tools for failed payment recovery. These systems can handle retries, send alerts, and even guide users through updating payment methods, all without needing your involvement.

Reduce friction at checkout: Ensure it’s easy for customers to update their details and complete a payment. Long forms, confusing layouts, or slow-loading pages can stop people from following through.

The Legal Side of Chasing Failed Payments

Before you reach out to a customer about a missed payment, it’s good to know what you’re allowed to do under the law.

Start by checking your terms and conditions: These should clearly explain how recurring payments work, what happens if a payment fails, and when a service might be paused or stopped. If these terms are clear and accepted at the time of purchase, you’re on solid ground.

Be careful with how you contact people: Use email or in-app messages first, and always maintain a polite and professional tone. You should avoid using aggressive language or making public posts that call out a customer, as this can lead to complaints or even legal trouble.

In most cases, small businesses don’t need to involve lawyers. But if large sums are involved or a customer has used services without paying and is refusing to settle, it may be time to speak with a legal expert.

If your business is subscription-based, you must follow data protection laws, especially if you’re storing or processing customer payment details. Tools that are PCI-compliant, such as Stripe or Razorpay, handle this for you.

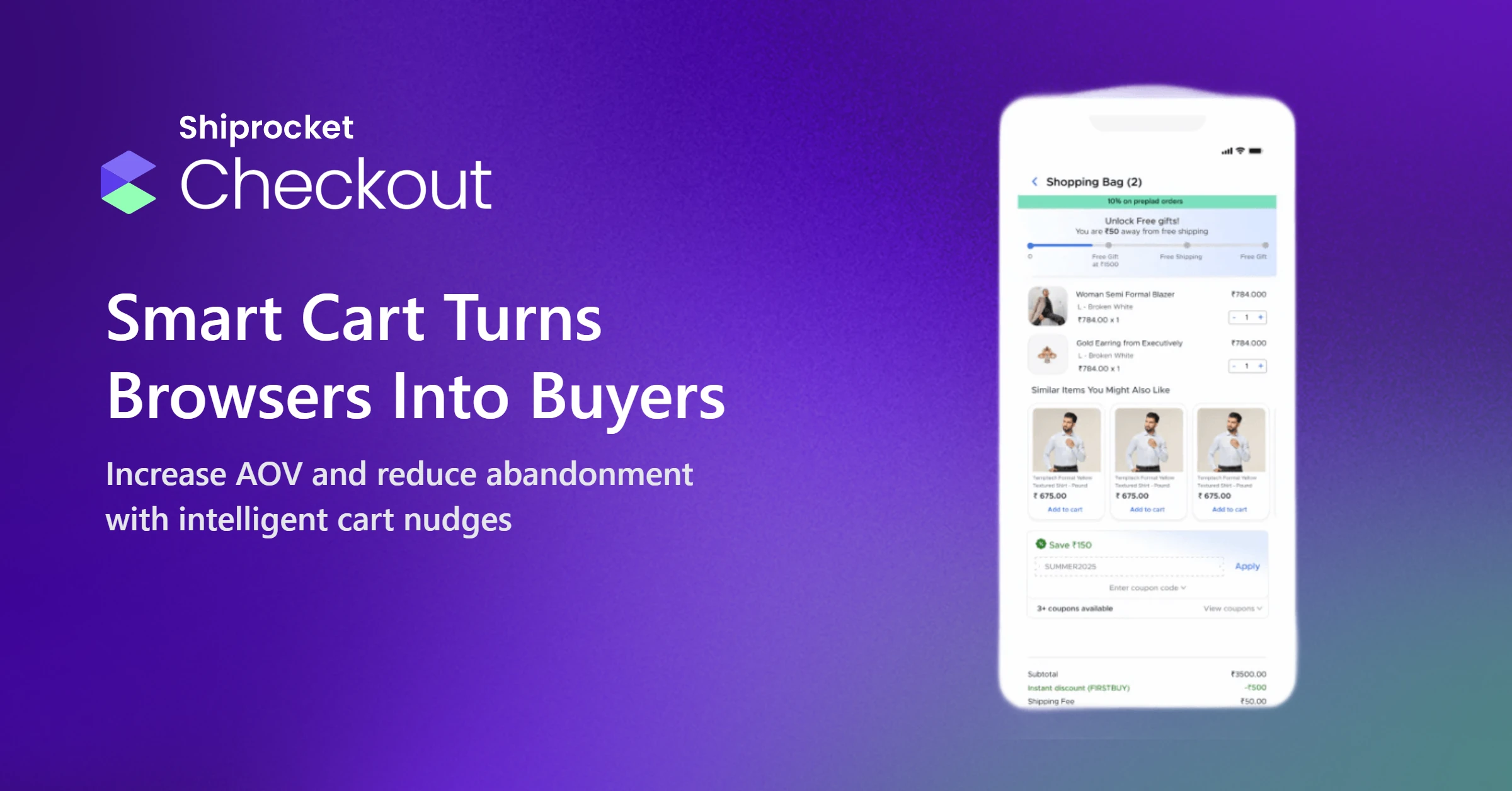

How to Streamline Payment Success with Shiprocket Checkout

One way to reduce failed payments is to make your checkout process smoother and smarter. That’s where Shiprocket Checkout can help.

This platform provides your customers with a fast and simple payment experience, supporting various payment modes, including credit and debit cards, UPI, wallets, and more. When you give buyers flexible payment method choices, they are less likely to drop off or encounter payment issues.

Shiprocket Checkout also helps with real-time tracking of failed payments. You can receive alerts, view detailed error messages, and quickly fix problems. If a payment fails, you can send customers a smart payment link so they can try again right away.

Another plus is that it’s designed to work well on both desktops and mobile devices. That means fewer issues caused by form errors, slow page loads, or failed redirects, which are common reasons for payments not going through.

And because Shiprocket works closely with logistics and order management, it provides better visibility across the entire customer journey, from checkout to delivery. That makes it easier to determine when payment issues are related to things like incorrect address data or cart errors.

Conclusion

Failed payments don’t just affect your income; they can even damage trust between you and your customers. That’s why it’s so important to treat these missed transactions as more than just technical errors. You can effectively recover from failed payments with the right setup, a clear process, and a friendly approach.

An all-in-one solution like Shiprocket Checkout can help you recover lost payments and make the customer experience smooth each time. You can turn a common business headache into a well-managed process by keeping your systems up to date, maintaining clear communication, and simplifying the payment process for your customers.